What FY22 may bring after COVID bust and boom

The impact of COVID-19 was sudden and unexpected, taking markets by surprise. As many investors will no doubt recall, many asset classes quickly dived amid extreme volatility in March 2020, the Aussie stock market crashing over 20 per cent over that month alone. But super fund members who held their nerve and did not panic have been rewarded with a year of outstanding returns.

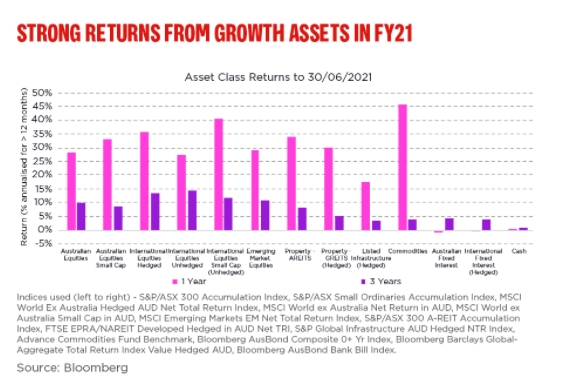

According to Chant West, the median growth fund was up 18 per cent for the year to June 2021, with many funds delivering returns in excess of 20 per cent. How did this happen following the quickest and sharpest recession since the 1930s?

A quick recap of FY21

It’s worth remembering that markets are forward looking. And by July 2020, the world was looking a lot better than it did a few months earlier. Individuals, communities, businesses and governments had come together, adapting to new social norms to keep each other safe and economies going.

Soon enough, this quickly turned into full blown economic recovery as lockdowns and restrictions eased, record government spending circulated through economies and vaccines emerged.

In the US, despite its lowest ever gross domestic product number at the start of 2020, the S&P 500 posted one of its strongest monthly returns since 1986 in August 2020 and Joe Biden’s Presidential election win in November proved a further positive turning point.

In Asia, a resurgence in cases in India towards the end of the financial year, along with soaring inflation due to heavy rainfall and increased energy costs, weighed on the recovery. But in China, all the share market losses since the start of the pandemic had already been erased back in October, with growth remaining strong.

Meanwhile in Europe, after Brexit terms were agreed in December 2020 the focus shifted to vaccine rollouts and economic recovery, while in the UK, a gradual exit from lockdown in April lifted consumer confidence as the country hurtled towards this month’s “Freedom Day”.

Finally, in Australia, after a rocky start to FY21, plenty of support from government stimulus (think JobKeeper) and the Reserve Bank’s record low cash rate of just 0.10 per cent – not to mention it joining the “quantitative easing” party (bond buying) – helped the economic recovery surprise basically all forecasters at every turn.

How did financial markets respond?

In turn, most major markets rallied hard, with several stock markets hitting record levels.

In particular, the Australian and US markets both experienced an extraordinary rebound following the economic policy support by provided by domestic and international governments.

While cash rates globally have been very low, or below zero since the start of the pandemic, cash and fixed interest unsurprisingly underperformed. But they still play an important defensive role in a diversified investment portfolio – providing some cushioning against large market falls, such as those experienced in March 2020.

Looking Ahead

Whist we still have governments and central banks rolling out stimulus to aid the recovery, we are conscious of the current impacts of second and third waves of the virus, now in many mutating forms such as the Delta strain taking hold across Australia, the UK, the US and other markets.

Understandably, this is starting to unnerve markets.

However, it’s likely we’ll see more stability in markets in FY22 compared to the previous 12 months as many major economies gain momentum.

In Australia, despite the current lockdowns, record low interest rates – which are not expected to rise until 2023 (at the earliest) – unemployment below pre-COVID levels and support from governments and the banks, means we are well placed to get through this recent challenging outbreak.

Globally, trade and territorial challenges with China along with ongoing tensions in the Middle East – in addition to the Biden administration exerting its influence across the globe – need to be monitored. And it was only a little over a year ago that the European Union was dealing with the reality of Brexit, with the impacts remaining unclear.

But stepping back, over the long-term both listed markets and unlisted assets, such as property and infrastructure, continue to provide good opportunities to build long-term wealth.

As always, maintaining good diversification in super when investing is key because it reduces the exposure to single economic or market “black swans” or events.

And by avoiding panic and staying invested for the long term, investors can make the most of rebounding markets – as FY21 showed in spades.